₹10 Lakh Investment Comparison: Bank vs Property – Which Builds Real Wealth?

Compare ₹10 lakh investment in bank vs property. Learn returns, risks, and which option helps you build long-term wealth in India.

3 min read

₹10 Lakh Investment Comparison: Bank vs Property – Which Builds Real Wealth?

When you have ₹10 lakh in hand, the question isn’t just where to put it—it’s about what kind of financial future you want to build. On one side, you have the safety and predictability of a bank. On the other, the growth potential and tangible value of real estate.

At first glance, both options may seem reasonable. But over time, the difference in outcomes can be significant. Let’s break this down in a practical, easy-to-understand way so you can make a smarter decision.

Understanding the Two Choices

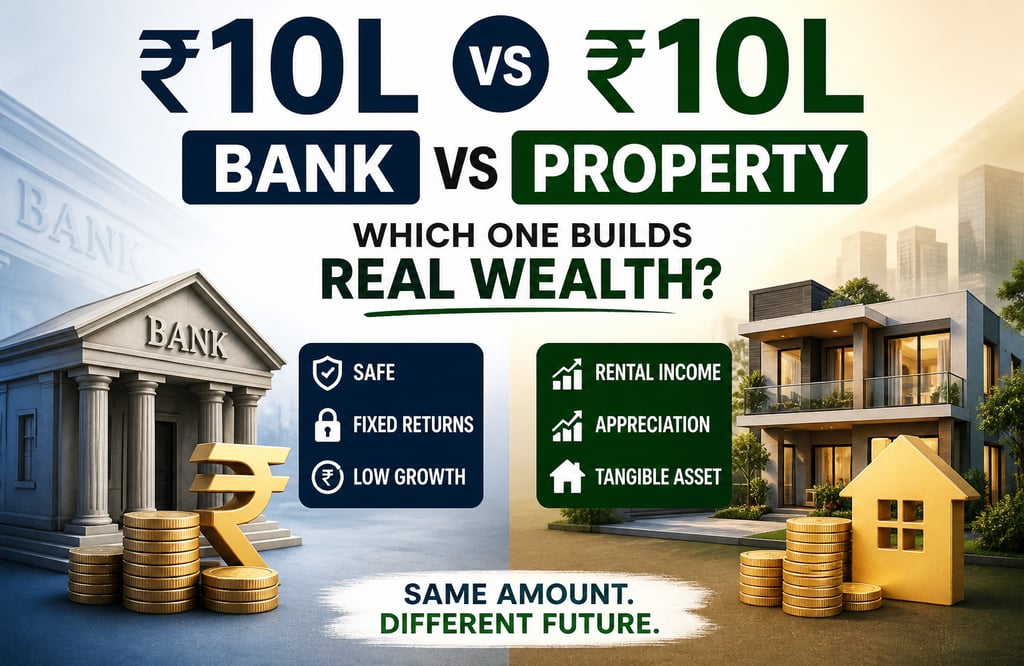

Option 1: Keeping ₹10L in a Bank

Most people instinctively choose to park money in a savings account or fixed deposit (FD). Why?

It feels safe

Returns are predictable

No active involvement needed

Typical returns:

Savings account: ~3–4% annually

Fixed deposit: ~6–7% annually

This means your ₹10 lakh grows slowly, but steadily.

Option 2: Investing ₹10L in Property

Real estate, especially through modern options like fractional ownership, has opened doors for investors with smaller budgets.

Here’s what property investment can offer:

Rental income (monthly cash flow)

Property appreciation (long-term growth)

Hedge against inflation

Unlike a bank account, your money is working in multiple ways here.

Growth Comparison Over Time

To truly understand the difference, let’s look at how ₹10 lakh can grow over 10 years in both scenarios.

Note: These are approximate figures to illustrate the difference, not guaranteed returns.

Breaking Down the Real Difference

1. Wealth Creation vs Wealth Preservation

A bank primarily helps you preserve money.

Real estate helps you grow wealth.

Bank:

Safe but limited upside

Property:

Higher growth potential over time

2. Passive Income Opportunity

With bank deposits, your income is limited to interest.

With property:

You can earn monthly rental income

This creates a second income stream

Even fractional ownership allows you to earn rental yields without owning an entire property.

3. Inflation Impact

Inflation quietly reduces the value of your money over time.

If inflation is ~6% and your bank return is ~6%, you’re barely breaking even.

Real estate typically outpaces inflation, helping you increase real purchasing power.

4. Tangible Asset Advantage

Money in a bank is just numbers on a screen.

Property:

Is a physical asset

Has intrinsic value

Can be used, leased, or sold

This psychological and practical advantage matters more than most people realize.

5. Risk vs Reward Reality

Let’s be clear—real estate is not risk-free.

Bank:

Very low risk

Guaranteed returns

Property:

Market fluctuations

Liquidity challenges

Requires research

However, with higher risk comes the potential for higher reward.

The Power of Compounding in Both Cases

Compounding works in both bank investments and real estate—but differently.

In Banks:

You earn interest on interest

Growth is steady but slow

In Property:

Value appreciates

Rental income adds to returns

Reinvestment multiplies gains

Over time, real estate can significantly outperform traditional savings.

Liquidity: A Key Consideration

One area where banks clearly win is liquidity.

Bank:

Instant access to money

Ideal for emergency funds

Property:

Takes time to sell

Less liquid

Smart strategy:

Use banks for short-term needs, property for long-term wealth.

Who Should Choose What?

Choose Bank If:

You want zero risk

You need quick access to funds

You’re saving for short-term goals

Choose Property If:

You’re thinking long-term (5–10+ years)

You want passive income

You aim to build real wealth

The Modern Twist: Fractional Ownership

Earlier, property investment required large capital. Today, that’s changing.

With fractional ownership:

You can invest with ₹10 lakh

Own a share of premium properties

Earn rental income proportionally

This bridges the gap between affordability and opportunity.

Real-Life Mindset Shift

Most people say:

“I’ll invest in property once I save more.”

But in reality:

Waiting delays wealth creation

Property prices keep rising

Opportunity cost increases

Starting early—even with ₹10 lakh—can make a big difference over time.

The Final Verdict

Both options serve a purpose. But they are not equal in outcome.

Bank = Safety + Stability

Property = Growth + Income + Asset Creation

If your goal is simply to protect your money, a bank works.

If your goal is to build wealth, real estate has a clear edge.

A Balanced Approach (Smart Strategy)

Instead of choosing one over the other, consider this:

Keep 20–30% in bank for safety and liquidity

Invest 70–80% in growth assets like property

This way, you get the best of both worlds.

Closing Thought

₹10 lakh is not a small amount. But its future depends entirely on how you use it.

The real question is:

Do you want your money to sit… or grow?

Because 10 years from now, the difference between the two choices won’t just be numbers—it will be your lifestyle, financial freedom, and opportunities.